The Imaginary Problem Of Congressional Stock Trading

Voters and commentators are united against what they view as a colossal grift. But what if they're wrong?

A ban on individual stock trading by members of Congress garners more support than perhaps any remotely contested issue in this polarized environment.

At a time when Democrats and Republicans generally can’t agree on the color of the sky, 87% of Republicans, 88% of Democrats, and 81% of independents would support a prohibition on trading by members of Congress in individual stocks.

The unity is seen in the media as well. In late February, Tucker Carlson interviewed Chris Josephs, developer of the Nancy Pelosi Stock Tracker account on Twitter/X. The tagline on YouTube: “Congress is even more corrupt than you may understand.”

Five weeks earlier, Alexandria Ocasio-Cortez (D-NY) appeared on The Weekly Show with Jon Stewart. Stewart and Carlson not only hold beliefs that are normally diametrically opposed, but famously traded insults on CNN’s Crossfire two decades ago. Yet Stewart, in an exchange with Ocasio-Cortez, echoed his adversary on this issue:

STEWART: They are on a committee. They get information about a drug or a contract or a thing. They immediately make a call. The stockbroker changes things, and their portfolio swells.

OCASIO-CORTEZ [correcting with emphasis]: Explodes. It explodes.

There’s even a level of unity in Congress itself. Last summer, lawmakers Jared Golden (D-ME) and Brian Fitzpatrick (R-PA) released a letter signed by 18 other representatives from both parties calling for a vote on a trading ban. In an accompanying press release, Golden laid out their position [emphasis ours]:

Members of Congress should be working in service of their constituents, not using their positions to line their own pockets. Personal stock portfolios do nothing to help our districts, and even the appearance of insider trading undermines faith in elected officials’ priorities. Anyone who feels the same should have no problem voting for this common sense, long overdue step.”

Indeed, a Congressional trading ban does, apparently, feel to the majority of Americans like “common sense”. The problem, however, is that there’s preciously thin evidence that stock trading by our politicians is even a problem to begin with.

The Current Regime

From a high level, it does seem unfair that elected representatives can trade stocks. After all, they have access to information that others don’t — what is usually considered “inside” information for people in other areas of the economy. They also regulate not just individual companies but the market itself, meaning there is the potential for significant conflicts of interest.

That said, Congressional stock trading is not unregulated. In 2012, the STOCK (Stop Trading on Congressional Knowledge) Act was signed after passing both houses with huge majorities. It prohibits trading by elected representatives using “any nonpublic information derived from the individual's position ... or gained from performance of the individual's duties, for personal benefit". Representatives also have to disclose any trades within 30 days.

To be sure, there are still huge concerns about this system. In 2023, Business Insider compiled a list of 78 members of Congress who had failed to comply with the STOCK Act. The “left-leaning” (per Wikipedia) Campaign Legal Center in 2022 called the act a “failed effort”. The CLC pointed out that the fine for disclosure violations was just $200 — with no further disclosure as to whether the fine was actually paid — and that argued enforcement of the act was effectively nonexistent.

But, at the very least, the idea that Congressional insider trading is allowed is not true. The issue now has become whether elected representatives should be allowed to trade stocks at all.

Burr And Pelosi Trade Their Way To Millions

In recent years, two political figures are no doubt most responsible for pushing the public to largely agree with the CLC.

The first is former Speaker of the House of Representatives Nancy Pelosi (D-CA). It’s not a coincidence that Josephs and his partners created a stock tracker under her name (as Josephs himself said to Carlson, it is a marketing effort). Pelosi’s massive growth in net worth over time has led to repeated allegations online that she almost by definition has profited from consistent, massive fraud. How else would she have a net worth of $250 million on a salary under $200,000 per year?

The other is former Senator Richard Burr (R-NC). In late January 2020, Burr began to receive briefings about the novel coronavirus pandemic. On January 31, he received “nonpublic information” on that topic from a source, according to a document from the Federal Bureau of Investigation used in support of a search warrant application. The same day, he sold $110,000 worth of stock. Less than two weeks later, he bought $1.2 million of Treasuries, which at the time (though perhaps not now!) were considered the ultimate safe haven during times of market and/or geopolitical turmoil. The next day, another $1.1 million in stock was dumped.

The FBI noted that Burr’s equity allocation went from 83 percent to 3 percent — an absolutely massive shift. It’s a shift that, barring inside information (and maybe even then), no credible financial adviser would ever recommend — particularly because (as Josephs noted in telling the story to Carlson) Burr was selling out of his retirement accounts. Making matters worse, Burr’s brother-in-law, Gerald Fauth, sold stock the day after Burr’s $1.1M sale, with FBI evidence showing Burr communicated both with his brother-in-law and the Senator’s sister the same day. According to a witness interviewed by the FBI, Fauth explained his decision to sell off shares by saying that he knew a senator.

(Some) Mitigating Factors Of The Burr Case

We’ll focus on Burr first, since his case is by far the largest roadblock to simply hand-waving Congressional trading activity away. It also probably had the widest reach, particularly because other members of Congress around the same time made seemingly questionably trades of their own.

And the case does seem like evidence that insider trading must be both widespread and fully tolerated by the rest of D.C. After all, Burr faced no consequences. He was investigated by the Department of Justice and the Securities and Exchange Commission, but neither acted. Partisan politics don’t explain that fact, either: the DoJ investigation was closed on the second-to-last day of Donald Trump’s first term; the SEC ended its probe in 2023, under the Biden Administration.

Meanwhile, given the evidence (a chunk of which did not come out until 2022, in response to lawsuits seeking unredacted documents related to the investigation), it is very hard to believe that Burr acted solely on public knowledge, as he claimed. At the least, the information he received as a senator certainly seems to have informed his trading. That trading had a significant effect: as the FBI noted, he made $164,000 in profits and avoided $87,000 in losses through the late January trades.

So to most observers, Burr violated the STOCK Act with no repercussions, which in turn makes it all the more likely that the current 5411 members of Congress are doing exactly the same. And while it’s hard to argue with that take, it’s worth considering a few aspects of the case that might add some nuance.

The first is that the disclosure regime, in this case, actually did work. Burr disclosed the trades. The media found out and covered the story aggressively; it indeed was a national scandal. And there were consequences, if even if they weren’t criminal.

Carlson, then at Fox News, called for Burr’s resignation. Burr had to give up his chairmanship of the Senate Intelligence Committee — a hugely powerful post — during the investigation. The senator had already announced, in 2016, that he would not run again in 2022. But the furor surrounding his trading probably would have ended his political career otherwise; at the very least, he would have faced a stiff primary challenge and then a tough re-election fight in North Carolina, then as now a ‘purple’ state.

So even without criminal charges, Burr did not just trade with impunity. There was a very real political cost — and for people in Washington, political costs quite often are more painful than financial ones.

The other issue is that there actually were financial costs here. It’s not clear exactly how the FBI calculated Burr’s profit and loss avoidance, but a look at the holdings sold suggests that Burr’s trades, over time, wound up costing him several hundred thousand dollars.

Bear in mind that by the end of 2020, the S&P 500 was up 13% from where it was when Burr exited. It’s not clear exactly how his portfolio would have performed (his disclosure only provides approximate ranges for the positions), but a review of his positions suggests he probably would have been in line with the index, and maybe done a bit better. He sold Federal Express, which profited from increased e-commerce and finished 2020 up 65% from where Burr exited, and 3M, which rose thanks to some help from protective personal equipment. Even the hotel company he divested, Extended Stay America, wound up doubling in about 16 months after it was acquired in a bidding war.

(It doesn’t appear, at least from disclosures, that Burr re-entered the equity market before his retirement in early 2023. That is not a surprise, given what the optics would have been of buying back in while still under investigation. But had he done so, there’s a scenario in which he would have lost even more, since U.S. stocks started falling in the spring of 2022.)

This is precisely why credible financial advisers don’t tell their clients to go from 83% allocation to equities to 3%. But, more seriously, this gets to an important point that is missed by critics of Congressional trading: information alone does not guarantee profit, which is all the more true for people who don’t have actual financial experience.

We =have a natural experiment to prove this point. In the early 2010s, across a period of years, a group of hackers were able to access 150,000 corporate press releases before publication, including quarterly earnings reports. Unsurprisingly, they profited — but not nearly to the extent that you might think. Having inside information about a coming pandemic — one of the biggest pieces of non-public information available to any American politician ever — would seem to offer the ability to make massive amounts of free money. Burr is proof that it isn’t.

What Exactly Are Our Representatives Buying?

It’s worth taking a step back as well, to understand the mechanism through which Senators and Representatives in theory could enrich themselves by crushing the market. A good place to start is the performance of the market as a whole.

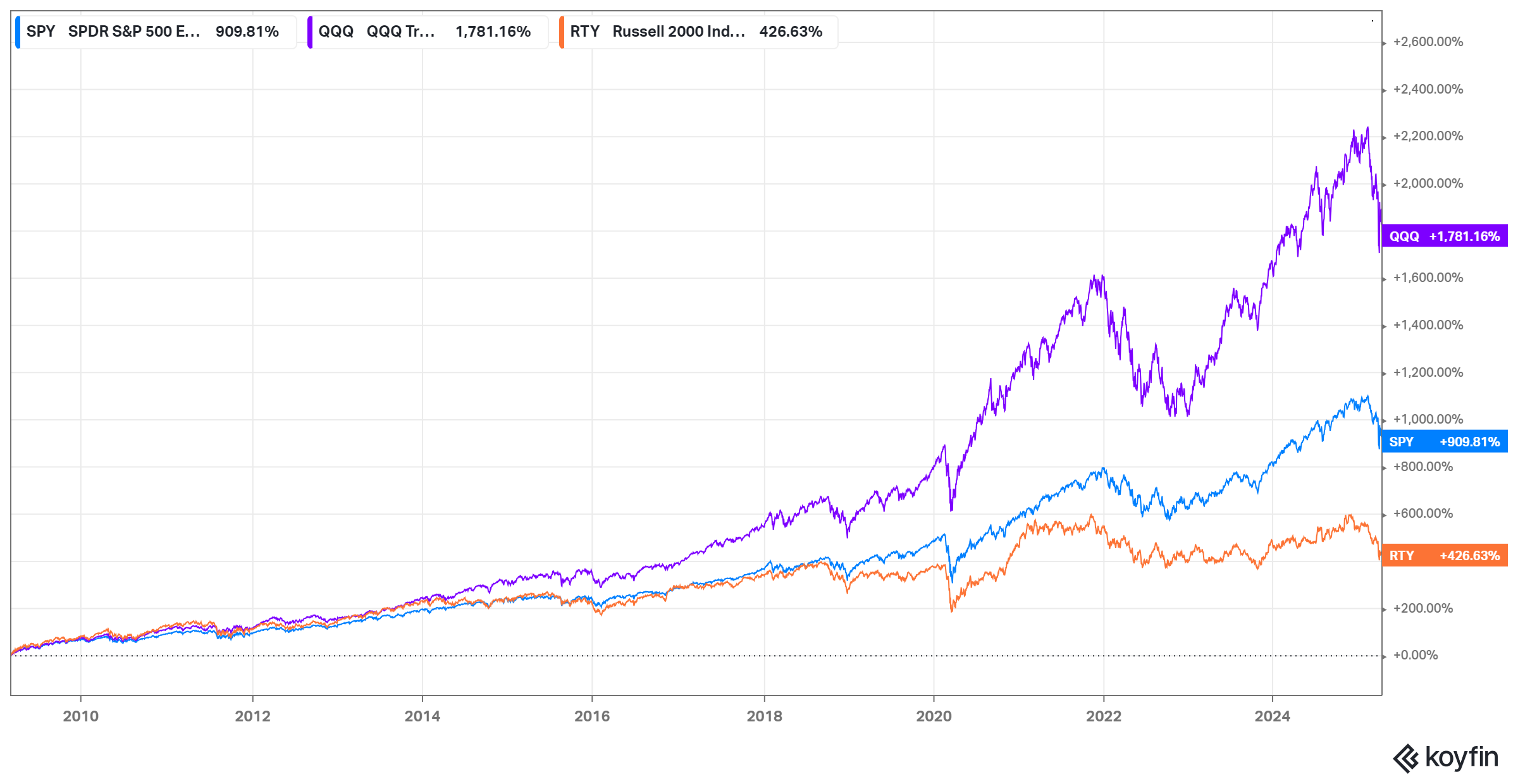

The U.S. stock market has performed spectacularly well over the past sixteen years. The Standard & Poor’s 500 index2 bottomed on March 6, 2009. Since that point, including dividends it has returned over 900%.

That massive gain alone colors the perception of the Congressional trading problem. It sounds ridiculous that, say, Nancy Pelosi could see her net worth go from $30 million in 2009 to the estimated $250 million now. How could she get so rich so fast without doing something untoward? But the value of all kinds of assets, and particularly U.S. stocks, have exploded since the financial crisis. Yes, Pelosi got richer in the market of the last 16 years. So did most investors.

But it’s also worth reviewing how those gains have come about:

source: Koyfin

‘SPY’ (blue) in the chart is the ticker for the largest index fund that tracks the S&P 500. ‘QQQ’ (purple) is the index fund for the NASDAQ 100, which leans more to tech and in particular, given its smaller universe of companies, “Big Tech”. ‘RTY’ (orange) is the Russell 2000, which is a larger universe that thus includes an incremental 1,500 smaller companies relative to the S&P 500.

What this chart reflects is a well-known and widely-discussed phenomenon in equities since the financial crisis, which is that gains have been much greater in larger stocks. (The chart even understates the point: those large companies at this point have a material impact even on broader indices such as the Russell 2000.) This trend peaked in 2024. The S&P 500 rose 23% for the year — but more than half of the gains came from just the market’s (and the index’s) seven most valuable stocks3, nicknamed the “Magnificent 7” by a Wall Street analyst.

This trend significantly undercuts the likelihood of widespread corruption, because the market as a whole is being driven by companies that, for two reasons, politicians literally can’t insider trade.

First off, these companies are essentially private sector actors; government spending and approvals simply don’t move the needle at all. That was true even for JEDI, the largest cloud computing contract ever awarded by the U.S. government. When Microsoft was named the winner of the contract over Amazon after a hotly contested battle, financial website Seeking Alpha noted the decision was “a bit of an upset”. In response, Microsoft stock jumped a whopping 2%, and Amazon fell 1%. Advance knowledge of who won one of the biggest awards in government history was worth hardly anything at all.

Secondly, for companies of this size — which, again, are the companies that have driven the entire market over the past 15 years — there isn’t really any information that is all that valuable. Online, you can see claims that Pelosi’s investment in Nvidia benefited from inside information that the Biden Administration would subsidize the semiconductor industry. That case doesn’t hold up: any “inside information” had to have occurred within two years of public debate over the bill that would become the CHIPS Act, a bill which saw repeated stops and starts. The sector moved higher throughout that period, because what is driving its growth is not federal subsidies created by the government, but rising global demand created mostly by the private sector.

Even earnings reports from these companies, which only happen four times a year, generally drive only a 2% or 3% move4. These large stocks — and many others — simply don’t have discrete events that can drive massive moves.

What’s notable about Pelosi’s disclosures, in particular, is how concentrated her trades (or, more accurately, the trades executed by her husband Paul Pelosi) are in precisely these names. They are almost without exception the biggest companies in the market, with a focus on tech: Microsoft, Amazon, Nvidia, Disney. Again, these are companies with a) minimal, if any, reliance on the federal government and b) companies that are so large that there is not real opportunity for inside information to move the needle.

In fact, it’s hard to even create a hypothetical piece of information Nancy Pelosi could gain from being a congresswoman that would help Paul Pelosi trade these names. These stocks do not trade on information that a congresswoman gets; they don’t really trade on individual pieces of information that anyone gets, but rather on their own execution over time and important, broader, secular, global trends.

Meanwhile, Paul Pelosi has been a successful investor for decades, and built up a real estate and venture capital investing business as well. In the equity market, his strategy does not seem to have changed all that much: his 2007 portfolio sounds much like the 2025 portfolio (though he has shifted further to tech of late). Paul Pelosi, per disclosures, also uses stock options, which generally increase both reward and risk.

So even a cursory look at the Pelosi portfolio shows that it is dominated by precisely the opposite of the companies where, as Stewart put it, a congressperson could “get information about a drug or a contract or a thing”. It is also dominated by precisely the companies that have driven the entire market higher over the past fifteen years. It’s no surprise — none — that their net worth has skyrocketed.

Indeed, in the context of the trading strategies here and the U.S. stock market, the almost unquestioned explanation here is simple. For 15 years (at least), Paul Pelosi, who has spent his professional life in varying areas of finance, has bet, and occasionally bet big, on the continued rise of Big Tech. That bet was correct — and it has paid off.

Where Is The Evidence?

It’s also worth looking more closely at Congressional stock portfolios. If the corruption was so widespread, and trading on inside information (or even maybe not quite inside but still helpful) such a source of profit, then the evidence would be overwhelming. Our representatives would be getting rich, there would be obvious trades ahead of drug approvals or government contracts, and overall Congressional trading would be hugely successful.

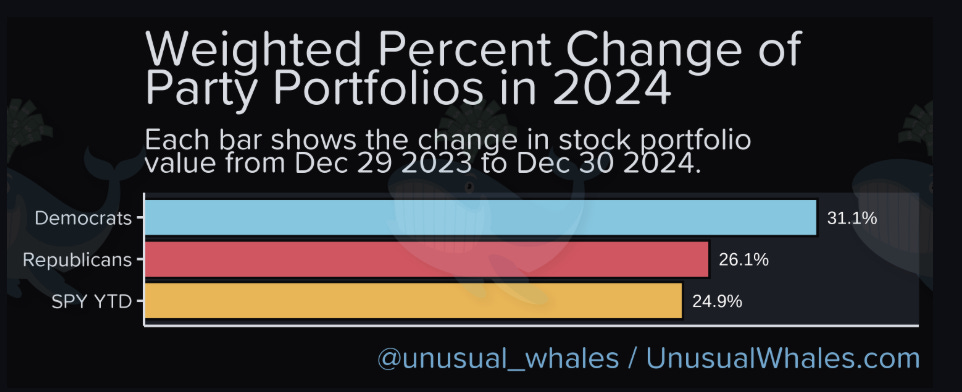

The latter point is what CongressTrading.com or Autopilot would have you believe. (Autopilot is the app from the team behind the Pelosi tracker; it allows you to copy a range of portfolios, including those of politicians, with Pelosi of course included.) So if you trade like a politician, you can profit. In 2024, that was the case, if modestly:

Source: Unusual Whales

A few hundred basis points (ie, a couple of percentage points) is potentially material. But as the site itself notes, and as we wrote above, while hyping up specific supposedly questionable trades, “Congress often held big tech, the winners of this cycle.” Only half of Congresspeople actually beat the S&P at all, which significantly undercuts the argument that insider trading is rampant or even common.

If you go to 2023, Congress as a whole narrowly beat the index. Again, tech was a factor. 2022 looks much better for the politicians, which held up against a 20% decline in the broad index, but there the calculations by Unusual Whales appear to be a factor (they only used trades actually executed in 2022, which means there was a chunk executed toward the end of the year, at which point the market already had started to rally).

But overall, there really isn’t much evidence that members of Congress are that effective. What outperformance we can see is somewhat inexact and also at least partially explainable by the fact that representatives lean toward tech and/or large-cap names. In the overall results, there certainly is minimal, if any, evidence of widespread corruption, or of repeated moves of the sort that Burr allegedly committed.

As for the allegations that everyone in Congress is getting rich, they seem based at least in part of flat-out lies about net worth promoted on social media (see here, here, and here). There are quite a few millionaires in Congress — just over half of the House and Senate combined, according to one tracker — but that’s not surprising. U.S. politics still selects for wealth, many spouses also work at six-figure jobs, and the Congressional salary of $174,000 per year is not nothing (particularly given that more well-known politicians can find other sources of income).

And, again, the stock market has cooperated: if you had $200,000 invested in an index fund in early 2009, you’re almost certainly a millionaire now.

Where Are All The Bad Trades?

The other issue is that for all the allegations that insider and/or unethical trades are common, no one really seems to be able to point the finger at any individually unethical trade that has actually occurred. Burr’s move is an exception here, admittedly. Right-wing media noted last year that Paul Pelosi sold Visa stock last year a few weeks before the DoJ launched an antitrust suit. But Pelosi is an active trader; simple math means eventually he’d hit an unusual trade or two. And there, too, trading inside information wouldn’t have even worked: Visa fell 5% on the news, and has promptly gained more than 20% since.

Indeed, if you actually go to the Nancy Pelosi Stock Tracker or Unusual Whales, there are a lot of trades that are meant to sound unsavory but actually fall apart on closer examination. The X ad from CongressTrading.com doesn’t even reference insider trading; it shows a contentious exchange from 2011 between Pelosi and 60 Minutes correspondent Steve Kroft over the Pelosis buying into the Visa initial public offering. (Stocks don’t trade before the initial public offering; that’s why the offering is ‘initial’.)

So there’s one buy highlighted of satellite play Viasat, purchased by Debbie Wasserman Schultz (D-FL). The account notes that Schultz bought the stock, after which point it received a “$500 million new military contract”, a $4.8 billion contract, and a $3.5 million task order as well. The stock at the time was up 62% since Schultz filed the buy.

Except the $500M contract wasn’t new, but a renewal of an existing deal; Viasat only got a piece of the $4.8 billion; and the $3.5 million is nothing in the context of $4.5 billion in annual revenue. Viasat also has a ton of debt, which makes its stock more volatile; a 62% move in the context of a raging bull market (this was before the tariffs) was not a surprise. And, indeed, the stock has given back most of the gains made in this “suspicious” trade.

This is not an exception. Quiver Quantitative in January posted a video of “one of the most suspect trades made by a member of Congress.” The trade by Michael McCaul (R-TX)5 was a buy of up to $100,000 in cybersecurity company Fortinet.

The video notes that McCaul a) is a member of the Cybersecurity Caucus and b) is pushing for the PIVOTT Act, which aims to fund scholarships for degrees given in return for government service. And the supposedly suspicious aspect is that Fortinet is lobbying for the program; the implication is that McCaul is in turn doing their bidding.

Except for the fact that absolutely everybody in the entire f-ing industry is lobbying for this act (except, at least according to this press release, Fortinet):

More importantly, Fortinet has a market capitalization of $75 billion. What is an army of experienced coders who have to go work for the government first worth to the company? Maybe a couple million dollars a year, if you really stretch? If the PIVOTT Act got passed, few if any investors would even care.

You can go on and on (while also noting that even those accounts highlight maybe a trade a month). There’s a Florida senator’s supposed connection to the gaming monopoly in her state, which ignores the fact that the monopoly is based on tribal gaming compact not her own intervention, and that a new federal bill would probably cost the sports betting industry money rather than help its growth. And there are a number of very basic financial mistakes made in the feeds that suggest limited if any industry experience6.

We could spend many more paragraphs dissecting relatively poor analysis, but the simple and more important question is: where are the obviously suspicious trades? Unusual Trades notes that over 10,000 Congressional trades are disclosed each year. If the perception of Congressional stock trading is anywhere close to the reality, there should be dozens, if not hundreds, of scandalous moves every year. Yet the people following it closely can do nothing but find vague, tenuous, immaterial, and/or misunderstood connections. If there is no smoke, where the hell is the fire?

Costs And Benefits

Admittedly, a reader could agree with all this and still believe that stock trading by members of Congress should be banned. It’s not just a matter of profiting off inside information, but the potential for conflict of interest. This was the heart of the matter in the exchange between Pelosi and Kroft, and comes up occasionally elsewhere, such as when members of Congress are deciding on whether to ban TikTok while owning shares of Meta Platforms (formerly known as Facebook).

There’s also an argument that perhaps the most suspicious trades aren’t being disclosed. The Burr saga goes against that argument; surely, he knew that disclosure would create some kind of negative publicity and he did it anyway. But if there is in fact this hidden web of duplicitous trades under a regime with no enforcement, it’s hard to see how adding another law banning trading makes any difference for people who are already flouting the existing rules.

But it does matter to those politicians who aren’t making unethical trades, which appears to be a majority, even according to the most ardent proponents of a ban. Telling wealthy people that they can’t manage their own money at all (some proposal include the ability to operate a blind trust, which still keeps the Congressperson out of the loop) if they run for Congress creates a pretty significant impediment. Maybe getting millionaires out of Congress is a feature rather than a bug for some, but this hardly seems like the way to do it. Even for less-wealthy but still-millionaire representatives, the right to financial self-determination seems important (and very American); removing that right requires much more evidence of a problem than we actually have.

And the fact of the matter is that we have very little evidence of a systemic problem. We have one notable incident from 2020, a few possibly problematic trades around the same time, and occasional stitched-together narratives that fall apart on any kind of close consideration. Even the 78 instances of STOCK Act violations compiled by Business Insider pretty much entirely include late disclosures; not ideal, certainly, but hardly the sign of entrenched corruption.

Congress has its share of problems, and its constituents no shortage of frustrations, but arguing that corrupt stock trading is a key issue simply ignores the underlying causes (among them the often-contradictory desires of those constituents themselves). And there’s something untoward, at least, about constantly creating vague implicit or explicit allegations of corruption, and then arguing that a ban on Congressional trading would “restore public trust”.

It’s not our representatives who are eroding that trust, at least not here. Rather, the people most undermining that trust are people who call out “suspect” trades with no understanding of how the stock market actually works, or commentators like Stewart who publicly allege mass corruption with literally not one single piece of evidence7. Congress doesn’t need to stop trading. They need to stop talking.

As of this writing, Vince Martin is long index funds that track the Standard & Poor’s 500. He has no positions in any other companies or securities mentioned. If you enjoyed this piece, give us a ‘like’ to both steer future content and to help us spread the word. Thanks for reading!

That’s the number from Congress itself, which includes five delegates from territories and the Resident Commissioner from Puerto Rico.

As we’ve written before, this index, commonly referred to as “the S&P”, pretty much includes the 500 most valuable public companies in the U.S. That description isn’t always exactly accurate but it’s easily close enough for our purposes.

The list is: Alphabet (the holding company for Google); Amazon; Apple; Meta Platforms (the owner of Facebook and Instagram); Microsoft; chipmaker Nvidia; and Tesla.

Tesla is something of an exception here generally, and today. As I write this, the stock has risen 8% after earnings. But that move is coming in a volatile market, and an environment in which the stock has become entwined in politics in a way that its fellow Mag7 stocks generally are not.

One point of credit: the people pushing the insider trading narrative professionally do aim to be bipartisan.

Josephs told Carlson he worked “in finance” at some point before moving to Bali and then becoming a snowboard instructor in New Hampshire.

This, unfortunately, is not new for Stewart. His credulous treatment of conspiracy theories around GameStop’s 2021 rally was equally devoid of factual basis.