Our apologies for failing to keep with the planned, more consistent structure. We’ll play a bit of catch-up in the coming days.

Today, we simply can’t read, write, or think one more word about the t-word this week, so we’ll focus on a pair of interesting, if potentially less apocalyptic pressing, financial matters this week.

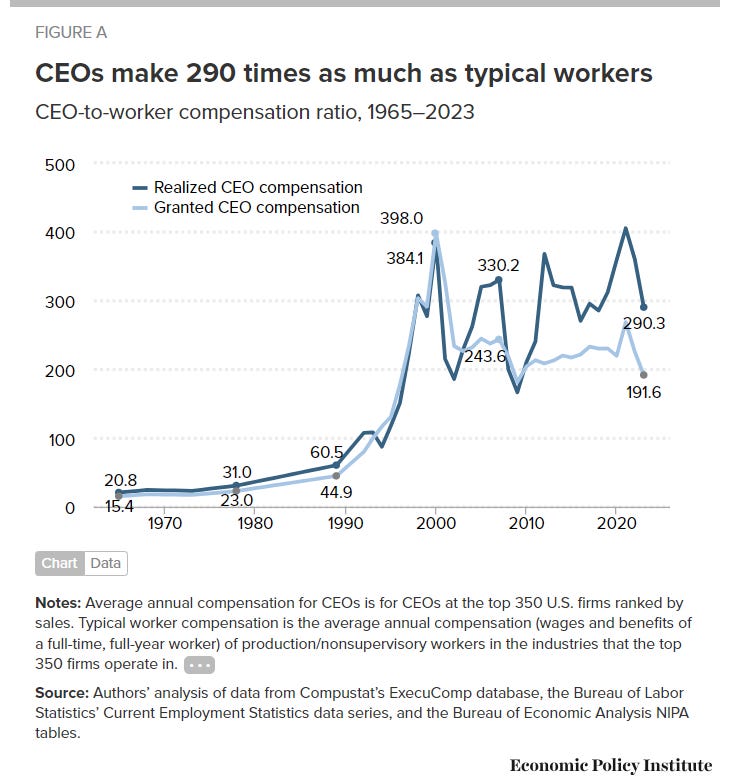

The Rise In CEO Pay

Over the past six decades or so, the pay (including salaries, bonus, and stock options) of corporate chief executive officers has exploded relative to the compensation of the average worker:

source: Economic Policy Institute

An interesting question is why. It seems like very few people, outside of the CEOs themselves, would want this outcome.

For progressives, this kind of income inequality is simply a non-starter. And even for small-c conservatives and/or hard-core capitalists, the rising gap doesn’t necessarily appear to be a good thing. Those capitalists do believe ardently in the rights of entrepreneurs to generate massive fortunes. The theory is that the potential to make billions of dollars drives risk-taking that in turn benefits society: Elon Musk’s fortune enables better electric cars, and Mark Zuckerberg’s the more efficient sharing of cat photos and conspiracy theories.

But capitalism doesn’t seem to require that managers, rather than founders, generate generational wealth without taking any real risk or moving society markedly forward. And many of those capitalists own shares in the companies that are paying these much larger compensation packages; to some degree, this higher CEO pay is coming out of their pockets.

Obviously, no politician would ever campaign on higher CEO pay; it’s an outcome that maybe a single-digit percentage of the voting population would be in favor of. And yet, here we are. Total annual compensation at S&P 500 companies1 in 2023 averaged $17.7 million. Setting aside charts and ratios, on its face that’s simply a staggering sum. Emotionally, it just seems unfair.

Yet we have some evidence that investors are fine with these seemingly exorbitant pay packages. U.S. public companies are required to hold an advisory (ie, non-binding) vote on executive compensation. Most shareholders are in favor. In the first half(ish) of 2024 (most of these votes take place between January and May), 98.8% of pay packages at S&P 500 companies were approved; the figure was actually slightly higher when moving to a larger universe that includes smaller public firms.

CEOs Matter

There are legitimate reasons why investors are content with compensating their chief executives so well2.

One is that the CEO job, particularly among the largest and most complex companies, is seen as being exceptionally difficult. I recently wound up talking with someone near the top of one of these S&P 500 companies (and who, I gathered, had deigns on reaching the CEO post in due time). With the help of some whiskey, I asked bluntly: would a reasonably intelligent, reasonably educated individual do that much worse than the average CEO? Did the job really matter that much?

The answers, if admittedly from a biased source, were two ardent ‘yeses’: a) that person would do much worse and b) yes, it does matter that much. Because it is hard.

A CEO has to understand the competitive landscape, inspire her employees, manage the expectations of and communicate with shareholders and Wall Street, guide product development, consider selling her company or buying someone else’s3, put out some fires and avoid starting others. And it is a job where getting one thing of many wrong — underestimating a competitor, leading a bad acquisition and/or entrance into a new market, or simply failing to communicate well to employees, shareholders, or the media — can have a material effect on profits and thus the stock price.

So, in this telling, if a company has a market value of, say, $50 billion, and one CEO is moderately better than another one, at least in theory that better CEO might well be worth a couple of billion dollars. And if a CEO is way better than another one would be, that ability has even greater value. Put simply, CEOs matter, and given that the S&P 500 at the moment is worth $50 trillion, plus or minus, total CEO compensation of ~$1 trillion (500 times the $17.7 milion average cited above), plus or minus, maybe isn’t that far out of line.

The second reason is more broad and more theoretical: equity investors are paying for aggressiveness. Owning stock in a company is more risky than owning its debt: shares of, say, Amazon AMZN 0.00%↑ might decline, but it’s exceptionally unlikely that the company will actually go bankrupt and fail to pay back its bonds. The flip side of that risk is that the rewards are much higher: Amazon stock can triple, but Amazon bonds cannot.

Shareholders thus would have rather have management take big swings: to use an extreme hypothetical example, a deal that either leads the stock to triple or wipes out the company is value-positive for shareholders, but value-negative for its bondholders (who are just fine if the company keeps selling stuff from China and building out its cloud business).

But those big swings need to be incentivized. Imagine a CEO of Amazon who gets $10 million a year in cash salary. Her personal incentive is pretty much to not get fired, because $10 million a year in cash is damn fine work if you can get it4. Even, say, a 20% bonus if the stock rises 25% in a year doesn’t necessarily change the calculus for her.

So U.S. corporations, in particular, have swung to issuing stock options to their executives to encourage risk-taking:

source: Tesla proxy statement, 2019 (author highlighting)

As that document (and many others) plainly states, the point is to match the incentives of managers with the incentives of shareholders. In fact, “incentives” is probably the wrong term. The singular “incentive” is more correct, because at the end of the day the point is that shareholders only really want the share price to go up5, and they want managers to feel the exact same way.

The Risk Facing CEOs

Executive compensation packages now are a majority in stock and/or in stock options. Those securities in turn have to “vest”, meaning they become effective over a set period of years (think 25% of the options become effective every year for four years). And usually, though not always, they are tied to specific performance targets.

For some companies, the idea of aligning incentives is pure: more options vest as the company’s stock price goes up, which in turn creates exponential growth in actual compensation, since each of those options is worth more as the price goes up.6 For others, the company might have to hit profit or revenue targets, or even post improvements in ratios such as return on invested capital or return on assets7.

Again, this structure incentives managers to be, and to stay, aggressive. But in theory it also means that bad managers don’t get compensated. If a CEO gets a $150,000 cash salary and $5 million worth of options, the value of those options is calculated8 based on the strike price, the current price, and the odds of being exercised.

In other words, in theory, the executive could sell that package of options for $5 million, or an investment bank could build that package for $5 million (plus a generous fee, natch). The stock and/or stock options granted are valued as compensation at the best estimate of their present value, both in terms of reporting the compensation (for instance, for the chart at the top of this article) and in terms of accounting for that cost in the company’s income statement.

Of course, that present value is not guaranteed to be realized. If ABC stock trades at $20, and the executive receives a million options to buy the stock at $20, there’s pretty significant risk here. If the stock goes down, the executive receives nothing. The options are worthless; there’s no value in the ability to buy ABC stock at $20 if you can own it through an app (for free) at $15.

Now, it is possible to create some value along the way: if ABC went to $24 in the CEO’s first year, she might be able to cash out some stock before it tanked. (Indeed, there are a number of companies where executives and board directors make millions as the stock keeps falling.) If the compensation is in restricted stock — for instance, our CEO gets 1 million shares of stock after lasting three years in the job — the compensation might be lower than expected, but still material.

Still, you can see in theory see some degree of fairness. A CEO does a good job, the stock goes up, adding potentially billions of dollars in value for shareholders, and in turn gets (usually) a low to maybe mid-single-digit percentage of the value created. If the CEO does a poor job, her compensation is limited to her cash salary plus some perks9; that’s still excellent money to most of us, but likely a significant step down from the compensation in the previous job and certainly from the compensation the executive expected.

The Tesla Example

The perfect and perhaps most extreme example of how executive compensation currently works comes courtesy of likely the world’s most famous chief executive officer.

In 2018, Tesla’s board of directors granted Elon Musk a pay package that was valued at the time at $2.3 billion. It wound up, at the peak Tesla stock price, being worth more than $50 billion.

That amount of money sounds simply stupid — but Tesla’s market valuation over the next five years would rise more than $500 billion from a base of about $40 billion. (At one point, the stock had risen more than twenty-fold). If Musk was one of the few, and maybe only, CEOs who could have created that value (whatever one’s sense of his politics, there is a strong case that he is a uniquely incredible leader of businesses), then Tesla shareholders got a good deal: greater than 10:1 for their money.

And Musk was taking some risk, even ignoring the fact that, at the time, he owned 21.7% of a company that he would later claim was skirting bankruptcy at the time10. His salary, per Tesla’s 2019 proxy statement, was literally the California minimum wage, and the company wrote that “Mr. Musk…has never accepted and currently does not accept his salary.”

To be sure, most minimum wage earners are not billionaires, even in California. But Musk’s option package, though it had a huge present value (again, over $2 billion), was nowhere near guaranteed money. Musk didn’t get a single option until the company’s market capitalization hit $100 billion — an increase of about 150% — and profit and revenue targets were hit. At that point, he received options to buy 1% of the company. At each $50 billion increase in market cap (with the required revenue and profit targets rising), Musk got another 1% ownership.

For shareholders at the time, this probably seemed like a great deal. If Tesla stock doubled, they were still paying their CEO minimum wage (Musk, at least per the Tesla proxy, received no other compensation). So good a deal was it that, last year when a judge rejected the pay package on the basis that Tesla’s board was conflicted, shareholders were upset. Rather than feeling grateful for essentially a free $50 billion in stock11, they voted heavily to reinstate the package. (A Delaware judge blocked that package as well; Tesla is appealing.)

But you can also see why some people might see Musk’s pay as ridiculous on its face — and why his (admittedly extreme) example raises real questions about how CEOs are paid.

Again, Musk owned 20% of the company; as the market cap ballooned from $40 billion to $580 billion, his stake went from ~$8 billion to more than $100 billion. Does he really need another $50 billion-plus on top of that to be incentivized to work hard and take risks? If additional compensation was required, wouldn’t, say, $30 billion be enough — and why didn’t the board try and save its shareholders $20 billion, and why didn’t shareholders themselves push the board to do so?

In short, why this does job require so much money?

Why CEO Pay Might Be Inflated

There are some structural issues that suggest CEO compensation probably is higher than it needs to be.

The first is the collective action problem. The average shareholder might want the CEO’s pay to be lower — let’s say a $10 million or even $5 million average against a current $20 million. But even for an institutional shareholder that owns a significant amount of stock, it requires a tremendous amount of exertion to get that figure down. It takes contentious conversations with the board (which raise the risk of being shut out from future discussions), and if those fail, trying to raise the issue at an annual meeting (which might color a firm’s reputation with other companies). It’s simply not worth the effort.

The second is the principal-agent problem. The board of directors is elected to represent the shareholders. But they also have quarterly meetings (at least) with the CEO, which are often followed by dinners. They will usually like the CEO personally. And if a director pushes too hard on compensation, he might wind up being on the wrong side of the board debate, and lose a cushy job in the process (directors at some major companies earn more than $1 million in annual compensation for what is a part-time job).

And, of course, as always in finance, there are unintended consequences. Back in 1992, Bill Clinton made a campaign promise to cap the corporate deduction for executive compensation to $1 million a year. But, crucially, the law signed after Clinton was elected excluded performance compensation. And so companies switched compensation to stock options. (There is an excellent Planet Money episode on this phenomenon, along with a Politico retrospective, both from 2016.) As the Planet Money piece pointed out, at the time the cost of stock options was not accounted for in corporate earnings (this was later changed), and so to some extent boards saw the options as “free”.

Indeed, if you go back to the image above, you can see the pay ratio absolutely skyrocket at this point, right through the stock market crash of 2000-2001:

Obviously, this was the exact opposite of what Clinton intended: the point of his campaign promise was that CEOs already were overpaid (as that Politico piece notes, even in 1992 US automaker CEOs made about five times what their Japanese counterparts did — as those Japanese companies were running them over).

And though the compensation clearly ran out of control in the 1990s, it hasn’t been reined in; the pay ratio as reported on a granted basis has remained relatively stable. (A recent piece from the Wall Street Journal suggests a further rise in 2024, at least based on data disclosed so far.) On a realized basis, a strong bull market over most of the past 15 years means executives have probably earned more than boards expected, and a greater multiple to the salary of the average worker.

As crazy as those pay ratios sound, there is perhaps some logic to how much CEOs are compensated, even if the exact level might be inflated by the inefficient nature of, well, human beings. But the structure certainly isn’t perfect. Executives benefit when the entire market (or entire sectors) go up; the head of a software company across the 2010s could have earned more than $100 million even while leading a business that underperformed its peers. Bad CEOs might see stock options expire worthless, but when terminated they usually manage to get a “golden parachute” worth millions — because the legal expense created by actually firing a CEO “for cause”, and withholding those benefits, is itself likely to reach into the millions.

Even good CEOs can take a hit from factors outside their control; at the moment, realized CEO compensation in 2025 seems likely to be way below expectations, because the launch of t——ffs by the U.S. government has tanked the market.

To some CEOs, that situation no doubt seems completely unfair. But after the last three-plus decades, it’s unlikely they will receive much sympathy.

As of this writing, Vince Martin owns index funds that track the Standard & Poor’s 500. He has no positions in any other companies or securities mentioned.

As we’ve written before, the Standard & Poor’s 500 consists of basically the 500 biggest public companies in the United States. That’s not exactly true, but it’s a good enough description for our discussion here.

These votes include compensation for other so-called “C suite” officers, including chief financial officers. CFO compensation is still quite high, but notably lower than that of the CEO: on a median basis, going from ‘F’ to ‘E’ roughly triples your pay package.

This is not the CEO’s job alone; the responsibility technically belongs to the company’s board of directors. But those transactions absolutely do not occur without her assent, tacit or otherwise, and the process rarely even begins without the CEO playing a significant role. This is in part because at a good number of companies, the CEO is also the chairman of the board; at most others, she’s at least a member of that board and so part of acquisition discussions.

Institutional investors understand this incentive, because one of the long-running criticisms of the financial industry is that compensation is such that investment management employees, too, don’t want to get fired.

This in turn leads to “herding” behavior; if you follow everyone else, and your market goes down, your negative performance doesn’t stand out and your clients will likely forgive you. If you buck the trend and are wrong, however, your clients are probably headed somewhere else.

There are occasionally other considerations — think ESG (environmental, social and governance) investing — but they historically have been subordinate to the core mission of “stock go up”.

The value in an option comes from the difference between the actual stock price and the “strike price”, the price at which the stock can be sold in the option. If the option is at $50 per share and expires today, it’s worth $10 at $60, $30 at $80, and so on.

To oversimplify, those ratios refer to how much company a profit makes for every dollar it’s invested (return on invested capital) or every dollar in assets it owns (return on assets).

The calculation is not necessarily perfect — it requires predicting the future, and incorporates many variables — but the nature of the calculation is relatively settled (it usually includes the Black-Scholes calculation, which won its creators the Nobel Prize in 1997). It’s not as if different companies will have widely different methods of calculating the present value of those options.

CEOs do get golf memberships occasionally, personal use of the corporate jet, security in some cases, etc. These perks can have values that near or sometimes exceed $1 million a year.

There’s some dispute as to whether Musk’s assertion here is true, or somewhat exaggerated.

If Musk’s shares of Tesla purchased via those options were canceled, every other shareholder would see their percentage ownership in the company increase proportionally.