In Defense of Corporations, Part I: Socialist Groceries And Corporate Profits

A "public option" grocery store could work — but private entities are not the problem

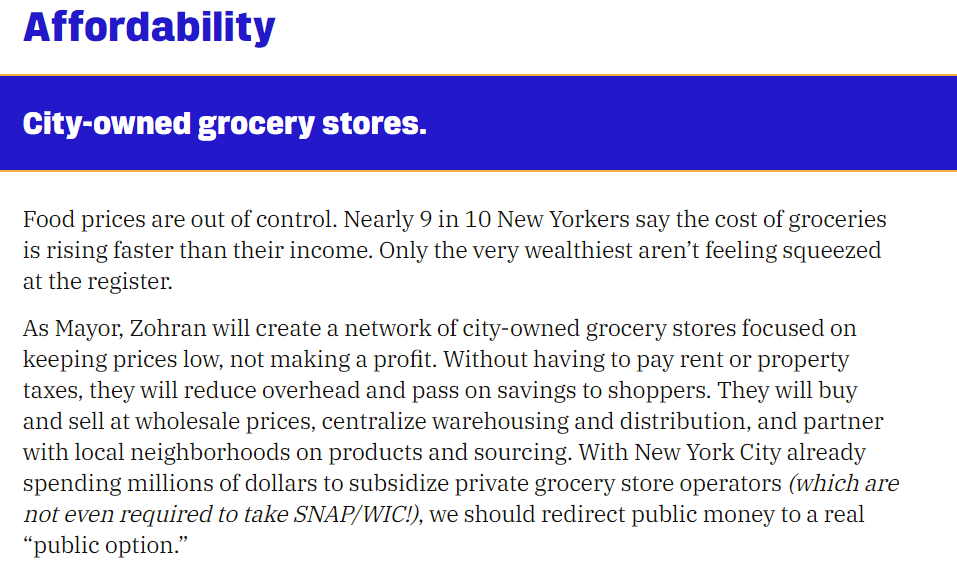

NYC Goes ‘Communist’

The surprise win of Zohran Mamdani in the Democratic primary for mayor of New York City has become national news. Millions of Americans whose understanding of the city comes largely from Seinfeld and Friends suddenly have a deeply vested stake in the outcome.

Outside of Mamdani’s views on the conflict between Israel and Palestine, none of his proposals seems to have garnered quite the attention as a plan to build city-owned grocery stores:

source: Zohran Mamdani campaign website

The arguments from the right have been unsurprisingly unrestrained: last week, the Wall Street Journal ran an op-ed (from the owner of a chain of private grocery stores in NYC) entitled “Want Soviet Bread Lines? Vote for Zohran Mamdani”.

It’s worth noting that, as is often the case, the attention massively outweighs the importance. Mamdani’s plan is a pilot plan that would open one store per borough for a total cost of about $60 million. It’s also not the first such project floated in the U.S.: Chicago and Atlanta already had such proposals (though Chicago eventually scrapped the idea). Nor is it anywhere close to Mamdani’s most influential proposal: policies toward rent-stabilized housing and broader taxation would have a far more significant effect on daily life in the city.

But the grocery store proposal is likely the most interesting. That’s not just because it is at least somewhat unusual, but because of what it tells us about what the left believes about capitalism, and (as we’ll discuss in a subsequent post) what most of us think of corporations.

Where’s The Margin?

The problem with Mamdani’s proposal is simple: grocery stores don’t actually make all that much money.

In fiscal 2024 (which ended February 1, 2025), Kroger, the nation’s largest grocer, posted an adjusted operating profit margin of 3.17%. Operating profit is what is left after essentially all expenses: the cost of buying product, the cost of running stores (including labor), rent expense, and depreciation (non-cash charges which smooth out capital investments in the stores). The figure here is not an outlier: Walmart posted margins of 4.4% in the same period (across the entire company; its grocery margins almost certainly are lower), and Albertsons was just below 3% adjusting for one-time costs.

Put another way, on the $170 in average household weekly spend on groceries, corporate profit accounts for maybe $6 of that figure. That’s not nothing — it is ~$300 a year, and in the higher-priced New York City market the figure might be $400-plus — but simply by definition supermarket profits are not the problem in the rising cost of food. Indeed, margins across the industry (adjusted for one-time effects and accounting charges around the treatment of inventory) haven’t really moved this decade, even as inflation has returned.

It’s possible, perhaps, to argue that the corporate problem exists further down the supply chain, but there’s not that much evidence there, either. Profit margins for major food suppliers like Kraft Heinz (21% over the last year) or Campbell Soup (14%) are much higher, but on a smaller share of overall grocery dollars. Nor have those margins jumped, either, despite claims from the left of “price gouging” particularly during and immediately after the novel coronavirus pandemic arrived in 2020.

Importantly, in terms of suppliers, it is quite clear that corporate concentration is not a problem, because the stock prices of those corporations have gone in the wrong direction. Over the last five years, even including dividends, the five most valuable U.S. packaged food companies1 have returned on average less than 2% over the entire period. The weakness in their share prices — based on investors’ total expectations of their future profits — are evidence that in sum their profits, and expected profits, haven’t grown at all. (In fact, adjusted for inflation, they’ve declined relatively sharply.)

Those major companies have seen their volume growth stall out, in large part because they are losing share to both smaller competitors and private label options. The former trend essentially disproves any concerns about monopoly or the ability to push out newer rivals. The latter trend has occurred because of shoppers adjusting to inflation by buying cheaper private-label goods, but also because grocers have been successfully pushing those options. And the ceiling on profit margins from food manufacturers has been driven in part by the negotiating power of grocers with scale against even the biggest suppliers. As we noted last month, oft-maligned Walmart is clearly the leader here, and its maniacal focus on low prices is both real and has ripple effects across the industry.

There’s a broader data point that applies far beyond the grocery space and discredits the supposed role of corporate concentration in driving prices higher. It’s difficult to remember now, but inflation in the 2010s (even in food) was actually below the target set by the Federal Reserve, leading to aggressive action not to lower inflation, but to prevent deflation. But of course, during the same prices were essentially stable, corporate concentration was increasing. (Kraft Heinz itself was the result of a 2015 merger between Kraft and Heinz which created, at the time, the fifth-largest food and beverage company in the world.)

And so the idea that the recent spike in inflation (which already has faded) was driven by corporate concentration/power/”price gouging” simply doesn’t hold up. As corporate concentration rose, prices did not. Even Nobel Prize-winning economist Paul Krugman — hardly a conservative — wrote last year of the “the popular but almost surely wrong view that corporate greed was the main driver of recent inflation”. At the very least, it’s not grocery stores that are the problem.

The Case For Mamdani

To be fair, some economists see it differently. In the New Yorker, John Cassidy gave a defense of what he called “Zohranomics”, leaning on a conversation with University of Massachusetts economist Isabella M. Weber. Weber has argued that major corporations did contribute to post-pandemic inflation — because they used external price shocks caused by supply chain disruptions and other factors as a way to pass along price increases and thus make more money.

In other words, the argument from Weber is basically that if corporate profit margins stay stable at a time of a price shock, then those corporations are contributing to inflation. If a grocery chain generates $100 billion in revenue and $3 billion in operating profit (3% margin), and then external inflation drives revenue up 20% to $120 billion, at the same 3% margin its operating profit too has jumped 20%, to $3.6 billion. In this telling, profit from the corporate entities ‘should’, absent some sort of intangible (and, to be honest, not-fully-explained) benefit of concentration, be closer to the original $3 billion — or else the corporate entity is taking advantage of the shock to increase profits.

It’s not an entirely ridiculous argument, though choosing a ‘correct’ operating profit level here between the pre-shock $3 billion and the stable-margin $3.6 billion seems arbitrary. (Is $3.2 billion OK? What about $3.4 billion?) But, regardless, the impact of profits on the actual increase is relatively small: assuming the grocer should keep no benefit from the external shock, and keep profit levels in dollars the same, the impact is 0.5% of the company’s total sales (in other words, 0.5% of total customer spend at the stores). One-half of a percentage point is not price gouging or anything close to it.

Even in that context it is, perhaps, fair to argue that a “public option” grocery store is worthwhile simply because it can save an average New York City family $500 a year. But the answer from the right is that it wouldn’t save money, because as the WSJ headline above suggests, public control means disastrous service, shortages, and higher prices. The common argument here is something along the lines of “do you want to shop with the same entity that operates the Department of Motor Vehicles (or the Post Office)?”

That criticism actually seems somewhat unfair. The Post Office does a pretty good job, to the point that something getting “lost in the mail” is seen as a bullshit excuse, not something that actually happens. And while the Post Office loses money, that’s because it operates many unprofitable offices which exist in rural (and, ahem ahem, usually right-leaning) areas.

The DMV isn’t terrible either; in Chicago of all places, it is fantastically run and incredibly efficient. Progressives could easily retort that that citizens don’t usually want services provided by Comcast or AT&T, either. The frustration of bureaucracy is caused far more by the need for and existence of bureaucracy, rather than the profit motive underlying the sprawling organization.

Corporations Do Good Stuff

All that said, a public option grocery store probably would wind up ‘losing’ some of those $400-$500 in savings per household. Its employees almost certainly would be unionized, against a current ~25% of New York City grocery workers. That would mean higher labor costs; given that ~9% of revenue goes to labor2, a 20% increase in labor expense for the public option would be ~1.8% of sales, wiping out probably half of the ‘savings’ generated by going the nonprofit route.

The idea of ‘free rent’ doesn’t really fly, either; it’s not ‘free’ to let an enterprise use a building that could have other productive uses (or be sold or leased). And a ‘public option’ would become a political lightning rod. Would a Mayor Mamdani be pressured to remove Israeli products from city-operated stores? Or to boycott Brawny paper towels and Dixie cups, which are manufactured by Georgia-Pacific, owned by the conservative-funding Koch Industries (and also probably not great from an environmental standpoint)? Given the ‘dual mandate’ argument for the stores to also provide protection from “food deserts” in underprivileged areas, should public-owned stores subsidize healthier foods — or not carry, for instance, high-sugar, low-nutrition Cap’n Crunch and Kit Kats?

Even assuming that a city-owned grocery can roughly match the efficiency of a private-operated rival (and that is a significant assumption, the DMV and USPS notwithstanding), there are real problems here. And there are real benefits lost as well. Grocers — yes, even big grocers — are really good at what they do.

Consider how rare the outbreak of food-borne illnesses is, despite the absolutely dizzying and pretty much incomprehensible supply chains that get food from the field to packaging to a shelf. Americans — even the poorest among us — have access to an absolute bounty of options from across the world, offered in (mostly) clean, (mostly) well-organized stores. The networks behind that, and the people behind that, are trained, expert, and experienced. Those networks aren’t perfect, and one can criticize the incentives that echo through the American food industry more broadly (those criticisms now come from the left and the right). But in the context of what consumers desire, and what Mamdani claims a public option could offer, the private sector is doing quite well at a reasonable (and stable) markup.

The idea that a city agency can simply and almost instantly build out capabilities in a manner anyway equivalent to those of Walmart or Kroger or even a local chain is somewhat ludicrous. At the very least, doing so requires tens of millions of dollars (a five-store, city-owned chain will need to pay up to poach experienced executives and managers from existing private chains; without experienced leadership and operational skill, the business will fail) and very real risk; again, it’s a pilot project. And that’s exactly the problem: no private enterprise would compete in such a complex, competitive industry without huge capital and a detailed plan to outperform rivals and capture market share. So far, it seems the plan here is basically “no rent and no profits”.

It’s tempting to believe that would be enough. It almost certainly isn’t. Where Mamdani’s idea falls truly flat is in underestimating the fact that corporations — even big corporations — do provide real value. The single-digit profit margin made by Kroger or an NYC chain like Gristedes isn’t just money being peeled away from tight-budget shoppers to aristocratic owners of the company’s equity. It is a return on investment, and a reward for what the company provides its shoppers — and the very fact that grocers succeed in a highly competitive environment proves that it is a reward that shoppers are willing to pay.

The problem is not necessarily that a city-owned alternative can’t provide the same reward. Given enough money, enough time, and enough backing, a “public option” potentially could have some level of success. The broader issue, and what Mamdani and so many on the left miss out on, is that there’s no need. New York City, and American, grocers, are quite successful already — for all of us.

As of this writing, Vince Martin has no positions in any companies or securities mentioned.

If you enjoyed this piece, give us a ‘like’ to both steer future content and to help us spread the word. Thanks for reading!

Kraft Heinz, General Mills, Kellanova (the former Kellogg without its cereal business, which was split off into a separate company because its growth had stalled out), spice manufacturer McCormick, and Hormel

That figure is from a study of independent and smaller grocers; commentary from Kroger suggests its figure is probably slightly lower, but most NYC groceries are run by smaller firms.