What The Market Tells Us About "Liberation Day"

Shaky math and a new definition of Trumpism

In our very first post we tried to add some context to calls for a tariff-driven “Trumpcession”. Predictions of a policy-driven recession, however, seem much simpler to make today. Global equity markets have plunged after President Donald Trump instituted tariffs on pretty much every country on Earth, plus some territories inhabited only by penguins.

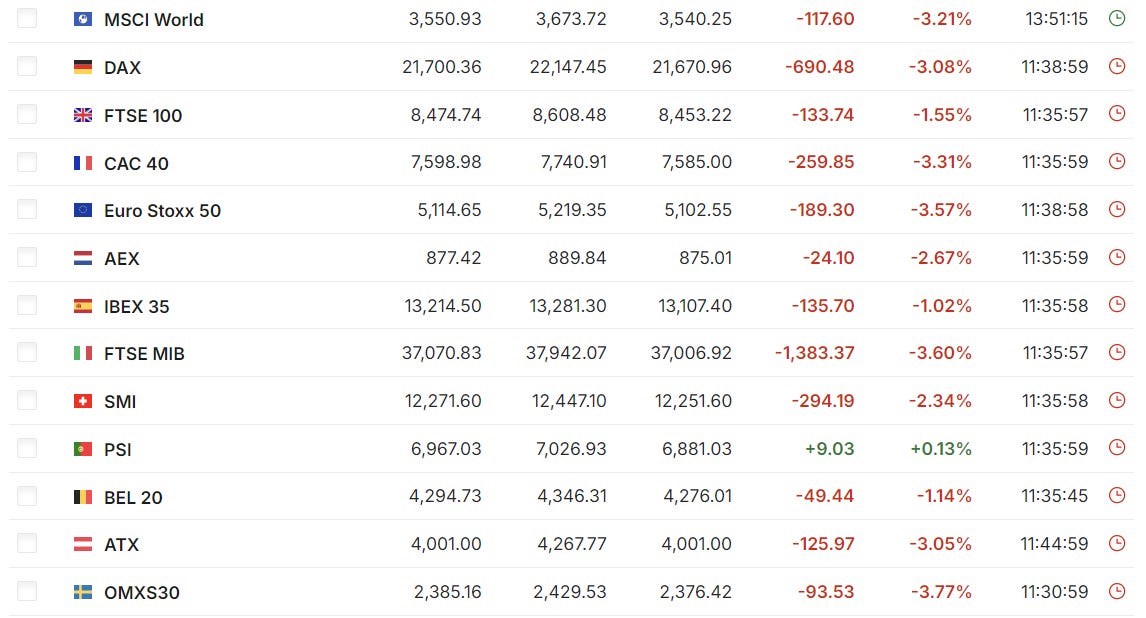

In afternoon trading, US indices are down 4%-5%, which alone represents a paper value loss of nearly $3 trillion. The news elsewhere too is negative, though not quite as bad:

source: Investing.com

To be fair, the fact that market indices are down is not necessarily a indictment of policy changes announced on “Liberation Day”.

A ~4% decline in the market’s expectations of total long-term profits generated by U.S. corporations (which is what, at least in theory, stock prices represent) doesn’t necessarily mean that investors are pricing in a recession. The trading could price in a shift in value away from corporate profits to employees or consumers. It could represent simple panic trading from an investor base trained on the incorrect economic that tariffs are prima facie poor policy. Or, the market could simply be wrong: Trump loyalists might point out that U.S. equities originally sold off after Trump’s first election was called in 2016, before seeing a massive reversal (though that reversal happened within in hours, a trend that has not repeated here).

Time will tell exactly who is right. In the meantime, there are some interesting lessons to draw.

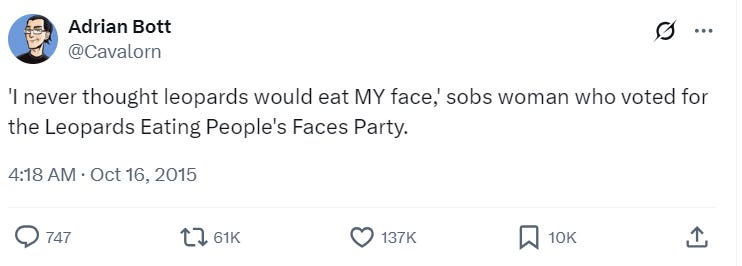

Markets Voted For the Leopards Eating People’s Faces Party

source: Twitter/X

One of the more famous posts on Twitter/X is this gem from 2015; it is “a parody of regretful voters who vote for cruel and unjust policies (and politicians) and are then surprised when their own lives become worse as a result.”

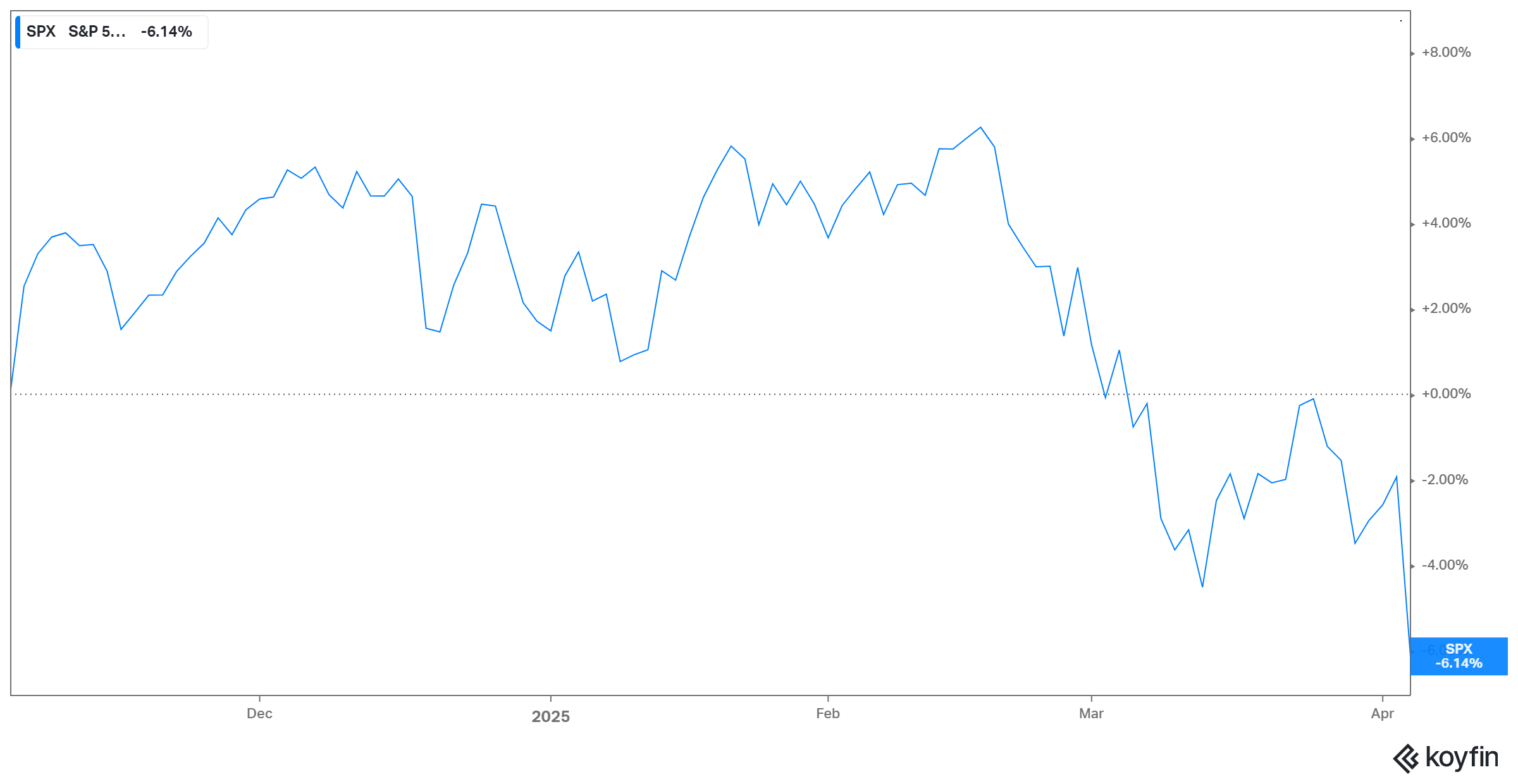

Thursday’s stock sell-off certainly looks like a similar moment for the U.S. equity market:

source: Koyfin

Markets cheered the Trump win in November, and kept buying U.S. stocks into February. The election wasn’t the only factor — optimism toward generative artificial intelligence was a major driver — but clearly, investors did not believe Trump on tariffs. Like many members of the Leopards Eating Faces Party, they heard essentially what they wanted to hear.

If you can look past the tumbling 401Ks, this is kind of funny. It also does suggest some sympathy for past leopard victims, such as the government workers laid off after voting for Trump. After all, the biggest equity investors on the planet misread the situation, despite likely having pipelines into the White House (through both Secretary of the Treasury Scott Bessent, a former hedge fund manager, and Secretary of Commerce Howard Lutnick, who ran an investment bank).

Trump Needs Belief

That said, the market’s inability to believe Trump on tariffs also creates a serious problem. Because the only way the Trump tariffs work for anyone is if they are in fact believed. The logic behind the tariffs, after all, is literally to remake world manufacturing, and that in turn requires trillions of dollars in investments over a decade at least, plus massive recruiting drives, supply chain shifts, and other significant moves. The mechanics of that — whether by a foreign company shifting production to the U.S., or a domestic company bringing manufacturing back — can’t even get started without real certainty that the tariffs are here to stay.

Despite the best efforts of the Trump Administration on Thursday to signal the president’s resolve, that certainty is nowhere close. One problem is that Trump and his Administration don’t appear to have figured out whether tariffs are good on their own, or whether they’re a useful negotiating tactic. Trump’s own speech highlights this contradiction: in one breath he’s saying to foreign countries, “terminate your own tariffs, drop your barriers” and get a reprieve, and in another he’s blaming the Great Depression on the 1913 introduction of the income tax and the subsequent shift away from tariffs. The former statement suggests room for compromise; the latter suggests no logic in even considering a compromise, as it implies tariffs are a prima facie positive.

The other problem is the haphazard way in which the tariffs were both instituted and calculated. During his second term, Trump already has reversed field on certain levies, sometimes within the same day. His commentary on the campaign trail was relatively consistent in actually applying tariffs, but provided little detail on how they would actually work.

Meanwhile, the math of the tariffs implemented is exceedingly questionable. White House officials tried dressing the numbers up in seemingly complicated math, but writer James Surowiecki seems to have been the first to figure it out. The administration essentially took the 2024 trade deficit for each nation, divided it by exports, and then halved the number to “be lenient”.

This is lunacy from a policy perspective, and even defies simple common sense. The formula only works if the idea is that trade deficits exist only because of “unfair” actions by trading partners, which in this case go beyond tariffs to unspecified “trade barriers” and “currency manipulation” (see the middle column of the the image below, underneath “Tariffs Charged to the U.S.A”):

source: Getty Images

That’s not the case: trade deficits can and do exist for many reasons, ranging from a partner’s level of economic development to its natural resources. Even setting aside the equally-asinine fact that the calculations exclude services (where the U.S. runs surpluses with pretty much everyone, thanks in part to the “Big Tech” firms so often criticized by Trump and his supporters), that creates a huge problem: there’s nothing that partners can do to “fix” this “problem”.

If a trade deficit is structural — if we, are for instance, importing quantities of a mineral that exists in small quantities here, or if the partner is offering us lower-cost goods without the economic ability to buy higher-dollar finished goods from us — it can’t be fixed by policy. Vietnam can’t get away from 46% tariffs by simply strengthening its currency (its central bank doesn’t necessarily have that kind of power, particularly against the dollar) or instructing its citizens or businesses to favor American goods.

In other words, the calculations are based on a hypothetical world where partners have far more control than they actually do. And that in turn undercuts the needed certainty that businesses and consumers will need to respond to these tariffs.

A French multinational considering establishing new production in the U.S. can’t just wait for its own government to respond to these new tariffs before making its decision. It has to weigh the French government response and then estimate whether that response will move the needle enough to satisfy the Trump Administration — even assuming the administration doesn’t lose its nerve ahead of, say, the 2026 midterms if a “stagflation” scenario arrives. Those calculations alone create enough uncertainty to provide a significant impediment to the changes the administration says it’s trying to implement.

What Individual Winners And Losers Mean

While markets on the whole did decline, there were some winners. 95 members of the Standard & Poor’s 500 (basically the 500 most valuable U.S.-based public companies; that description is not completely accurate but close enough for our purposes here) rose. The biggest winner was Lamb Weston, the manufacturer of French fries for McDonald’s; that company did also report quarterly earnings that contributed to its rise.

The market’s initial response does support those who criticize the tariffs on the thesis that it will hurt lower-income customers. Dollar General stock rose 4.7%; grocer Kroger rose 5.2%. Clearly, the market is pricing in greater profits for those companies, which in turn means higher prices. Somewhat ironically for anti-’green’ Trump supporters, First Solar, a U.S.-based manufacturer of solar panels, saw its shares jump nearly 5%1. Food stocks also gained; McDonald’s and Yum Brands (owner of Taco bell and KFC) rose 2%. We’re certainly seeing, at least initially, the market pricing in higher food inflation2.

The biggest losers in the S&P 500 centered on consumer tech and apparel, given higher tariffs on products from Asia (and thus higher prices). Dell was the worst name in the index, down 19%; retailer Best Buy plunged 18%, and HP (the former Hewlett-Packard) 15%. Nike and Ralph Lauren too declined double-digits. Similar trends exist in smaller companies, with apparel more broadly absolutely routed. In a direct rebuke to Trump’s speech, which highlighted unfair tariffs on motorcycles, Harley-Davidson stock fell 10% to a four-year low.

For now, at least, individual stock movements suggests the market as a whole believes tariff skeptics far more than it does the Administration.

A New Definition Of Trumpism

All told, there is real reason for concern here. At least initially, the equity market is projecting higher prices and lower profits; in other words, stagflation. The market may be wrong, certainly, but the inability of partners to necessarily (or simply) satisfy Trump Administration demands adds another potential stumbling block.

But there should be another takeaway here. Roughly a decade after he entered the American political scene3, it’s quite clear that we still don’t entirely understand what Trump believes or what ‘Trumpism’ is. Clearly, the financial markets have been wrong on that point, with U.S. equity indices down ~15% since it became clear in February that Trump was as serious about tariffs as his commentary suggested.

The problem seems to be that, because Trump has come from the Republican Party, Trumpism is defined as a different kind of conservatism. But this tariff move seems to confirm that Trumpism in fact is simply the mirror image of modern progressivism. Both movements believe strongly in structural unfairness driven by government and large corporations. Both are huge into the culture wars and virtue-signaling (those ‘MAGA’ hats don’t sell themselves, nor do the constant stream of T-shirts and bumper stickers with ‘1787’ or the Gadsden flag on them).

The difference, from the perspective of Trump and his supporters, is who the victims are. In their view, it’s white people, unfairly cheated by affirmative action policies; rural Americans, targeted and snickered at by urban elites; Americans as well, taken advantage of by rapacious foreign governments.

And this policy is an aggressive, activist, progressive intervention to fix that latter problem. The incredible irony is that the logic of the actual levies is pretty much identical to that of the DEI (diversity, equity, and inclusion) movement Trump so scorns. It is an effort to achieve precisely what conservatives scoff at liberals desiring: equality of outcome (the actual trade deficit) instead of equality of opportunity (the actual tariffs). And, like DEI, it assumes that the existence of disparities can be mostly, or in this case only, explained by structural unfairness.

When Trump said at the 2016 Republican National Convention that “I alone can fix it”, he sounded like an exceptionally liberal politicians. Nearly nine years later, he’s certainly acting like one.

As of this writing, Vince Martin owns shares of First Solar and index funds that track the S&P 500. He has no position in any other companies or securities mentioned.

Disclosure: I own shares of First Solar.

It’s also possible that investors shifted to those names, known as “defensive” names, because they do better in a more difficult macroeconomic environment. Of course, that’s not necessarily a vote in support of the tariffs, either.

At least in this iteration; Trump did run for the Reform Party nomination in 2000, losing out to Pat Buchanan.