WTF Is Going On: The CEO's Girlfriend, $2 Gas, And The Market Recovers

Why it's hard to get fired "for cause"; why the GOP should (quietly) own gas stations; and why tying the market to politics is a fool's errand

It’s Hard To Get Fired “For Cause”

In our piece last month on the pay of corporate chief executive officers, we noted that CEO compensation has shifted to line up with stock market returns. If the stock goes up, the CEO can get very, very rich; if it doesn’t, she ostensibly leaves with a small payout (at least by the standards of well-paid executives).

What we left out, largely due to length constraints, is that the downside here isn’t quite as significant as it would be in theory. If a CEO fails, she usually gets terminated at some point. That termination can be “for cause” — the executive essentially is getting fired — or “without cause”, meaning, broadly, that there are other factors at play (for instance, the board just wants a change, even if existing performance was not so substandard as to be intolerable).

CEOs fired “for cause” generally receive nothing, or close in terms of severance. In contrast, those fired “without cause” usually receive a package which might include a consulting arrangement with the company, health insurance payments, and/or accelerated vesting of existing stock options (ie, she can exercise options that contractually would not be exercisable until the future).

Often, these packages can be worth in excess of eight figures1. And they do create a bit of a “tails I win big, heads I don’t lose much” situation for the CEO. Even a CEO that does a terrible job (at least as measured by the stock price) can leave the position essentially set for life, albeit a life limited to travel in business class rather than via private jet.

Oddly, nearly all CEOs are technically terminated “without cause”, even if in most cases there is a clear cause: poor performance of the business and/or the stock. But as with the high pay of CEOs more generally, there is some logic to the fact that boards usually take this route.

For one, there are legal fees involved with firing “for cause”; nearly all CEOs will have enough in their favor to at least file a lawsuit claiming that their performance was good enough to avoid a termination. (Given the value of the severance package, most of them probably will file that lawsuit.) And that lawsuit will cost the company money; paying, let’s say, $3 million in legal fees to save on a $10 million package is not necessarily a great investment, particularly if there is any chance of actually losing in court. (Some disagree here: after buying the company, Elon Musk fired the executives of Twitter for cause, leading to a still-pending lawsuit.)

But more important is the fact that a CEO change, for any company, is a large disruption. As a result, firms want their former CEO to at least be around, if not in charge; the new CEO (who often comes from outside the business) should be able to reach out to her predecessor and understand the challenges of the business, the personalities of other top executives, etc. The board may well think the former CEO is a moron, but that moron still has value for a year or two while her replacement learns the ropes.

(Incidentally, this also explains to some extent the retention bonuses paid to executives of failed banks or bankrupt companies that so often arouse public outrage. It seems insane to pay more money to someone who ran a company into the ground. In some cases, those executives didn’t lead the company to its downfall, but instead arrived too late to save it. But either way, to mange bankruptcy a company desperately needs the knowledge of the people who know it best. Unfair as it may seems, those people are often the idiots who made terrible decisions and, who as a result, wind up with a great deal of negotiating leverage.)

There’s also the fact that the board of course hired the CEO in the first place. And it doesn’t look great for them personally to have hired someone who was so pitiful at the job that she had to be fired for the performance. It also cast doubts on the next hire: if the board’s vetting process is so poor as to allow one failure into the top spot, who is to say they won’t do it again?

The Kohl’s CEO And His Girlfriend

Overall, corporate boards are highly incentivized to make CEO transitions as seamless, painless, and relatively drama-free as possible. But on occasion, their hand is forced, and CEOs are fired for cause.

Nearly always, this requires a substantial ethical lapse. And it is somewhat comforting to note that often this ethical lapse involves sex. (CEOs are risking too much money and too much personal and professional happiness for the sake of getting laid: they’re just like us!)

Perhaps the most high-profile example in recent years came in late 2019. The CEO of McDonald’s, Steve Easterbrook, had probably one of the 200 best corporate jobs in the world and had done an excellent job in his position. But the board discovered that he had a consensual sexual relationship with a co-worker, and he was fired.

Incredibly, even that termination was originally designated as being without cause. But the board received a tip that Easterbrook had slept with multiple co-workers and sued; the former CEO eventually returned $105 million in stock awards and cash.

In that context, it was stunning when Kohl’s announced last week that its CEO Ashley Buchanan had been fired for cause. The department store chain has been reeling for years amid online competition; at the time, its stock was near its lowest point in almost 30 years. Add in the complexity and uncertainty driven by the new tariff regime, and under no circumstances would the board have considered moving on from a CEO — much less a CEO only hired in January.

In other words, Kohl’s had to have good reason — really good reason. The company’s filing with the U.S. Securities and Exchange Commission hinted at the issue:

Mr. Buchanan’s termination follows an investigation…during which it was found that Mr. Buchanan had directed that the Company conduct business with a vendor founded by an individual with whom Mr. Buchanan has a personal relationship on highly unusual terms favorable to the vendor and that he also caused the Company to enter into a multi-million dollar consulting agreement wherein the same individual was a part of the consulting team. It also found that in neither case did Mr. Buchanan disclose this relationship as required under Company’s Code of Ethics.

Helpful leaks would clarify the story. The Wall Street Journal reported that Buchanan had steered business to his girlfriend Chandra Holt. Like Buchanan, Holt has a long history as a retail executive; she was briefly the CEO of Bed Bath & Beyond as it headed into bankruptcy and eventual liquidation. The Journal — somewhat salaciously by its standards — cited messages from Buchanan’s divorce that proved he and Holt entered an extramarital affair.

Holt now runs a coffee business known as Incredibrew, though it’s not clear Kohl’s actually sold that product (it’s not on the website and Holt denied that she had “not received any compensation for my Incredibrew business from Kohl’s.” But Buchanan also steered business to Boston Consulting Group, where Holt worked. BCG fired Holt, according to the New York Post.

Bloomberg would follow up with its own reporting suggesting that the relationship between Holt and Buchanan dated back nearly a decade to when both worked at Wal-Mart, and was an “open secret among colleagues”.

The reporting of personal details by usually staid financial news outlets gets to how unusual this story is. CEOs sometimes sleep with their co-workers. They don’t usually turn people they are sleeping with into consultants and suppliers.

And the cost was absolutely huge — for both Holt and Buchanan. Holt lost her job; Buchanan must repay about $2.5 million, the pro-rated portion of a $3.75 million signing bonus. A $17 million grant of restricted stock already had turned into paper value of about $7 million as Kohl’s stock declined, but that, too, is real money.

All told, favoritism toward Holt — and, as the board noted, the failure to disclose that favoritism — cost Buchanan at least $10 million and his reputation. Succumbing to passion at the office — particularly for CEOs who often live at the office — is somewhat understandable. But this more premeditated error seems something different — why is why, perhaps, the financial press has so enjoyed covering the story.

Should The GOP Open Gas Stations?

President Donald Trump keeps saying that gasoline is under $2 per gallon. This does not appear to be true, which in turn means the U.S. public is once again playing the dismal game of “is our president lying or confused?”

There’s a case that Trump is actually mistaken. As CNBC noted, gasoline futures hit $1.98 per gallon around the time the president began making the $2 claim. It’s thus possible the president is confused between wholesale and retail pricing, though his insistence that the price has been reached in three different states somewhat dispels that interpretation.

But one does wonder if there isn’t an easy fix here. Could the GOP (obviously through some sort of ownership structure that would shield its involvement) or a wealthy supporter simply make his statement true?

Casey’s General Stores, a chain based mostly in the Midwest that focuses more on retail stores, sold an average of 1.1 million gallons per store in its most recent fiscal year. Murphy USA (which is connected to Walmart) does 240,000 gallons a month, or nearly 3 million gallons per store per year.

So a supporter could put three gas stations in rural areas in cheaper states like Arkansas and Oklahoma and offer $2 gas for a month. The station would lose about 70 cents per gallon at the moment — but on maybe 1 million gallons if the $2 price went for a month, even assuming traffic soared to take advantage of the offer.

That’s a $700,000 loss per station — or maybe $2 million. It would also be offset by presumably increased sales of in-store merchandise; each chain does nearly $1 million in annual gross profit (~$80K a month) beyond fuel.

All told, public data suggests it would cost about $500,000 per month to run $2 gas. Given that the two campaigns in 2024 spent a combined $3.5 billion, that seems like a reasonable investment to support the president and maybe tweak the opposing party.

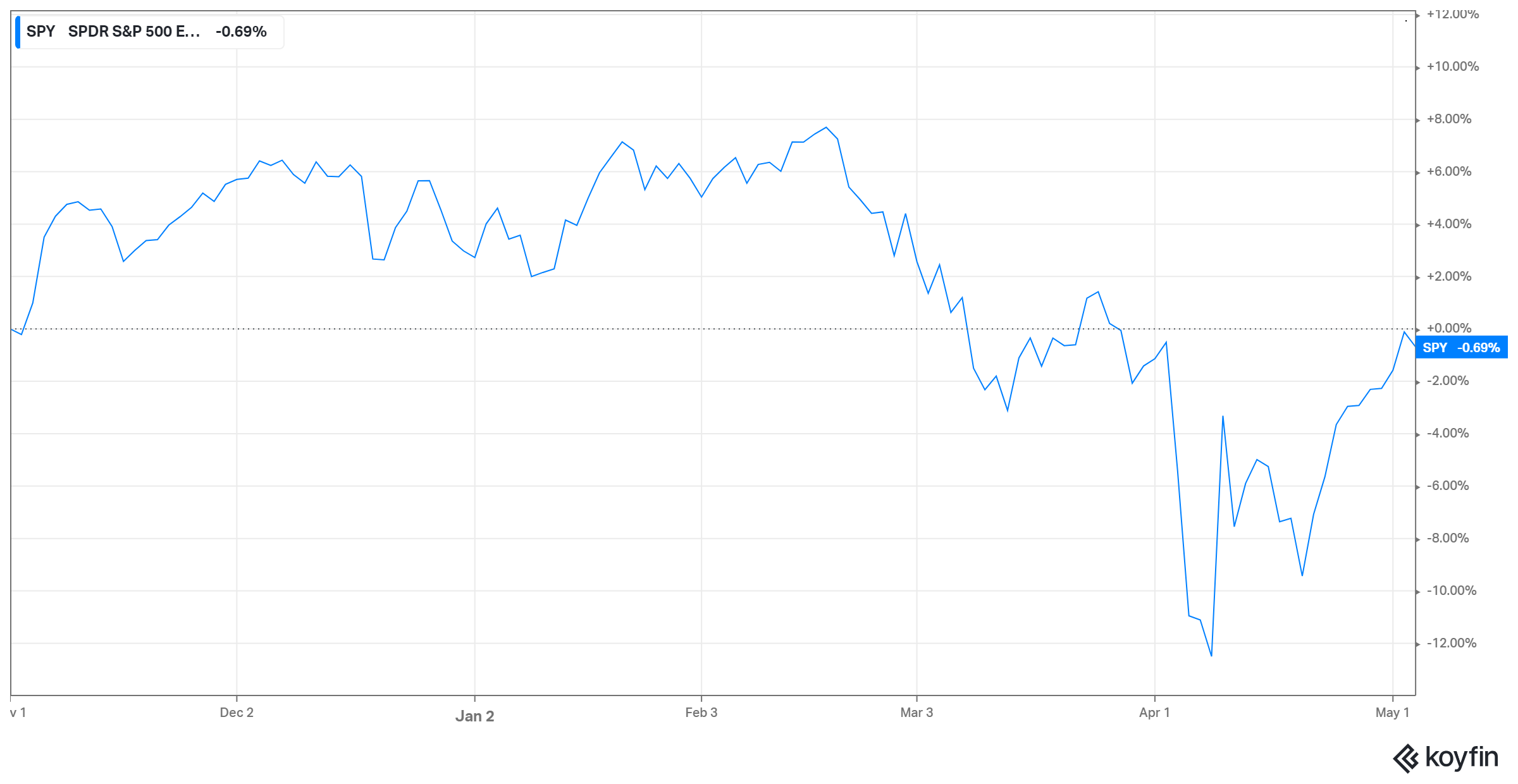

The Market Recovers

In our very first post, we cautioned against drawing sweeping conclusions from short-term stock market movements. And though that wasn’t investing advice, the market has recovered. The Standard & Poor’s 500 is now flat to where it was the day before “Liberation Day” on April 2 and to where it traded on November 1, days before the U.S. presidential election:

source: Koyfin

To be sure, that doesn’t mean the market suddenly has decided that tariffs are good — or, at least, neutral. The gain in U.S. stocks to at least some degree is driven by belief (hope?) that the broader tariff policy will be reversed. But it does show that the ‘story’ the market is telling is never simple. In investing or in politics, believing otherwise can make you look a little bit stupid.

As of this writing, Vince Martin has no positions in any companies or securities mentioned.

If you enjoyed this piece, give us a ‘like’ to both steer future content and to help us spread the word. Thanks for reading!

This is not quite a “golden parachute”, which usually refers to the payment received by executives who sell the company. Those packages, technically known as “change in control” provisions, are meant to incentivize the executive to sell the company in a deal that’s good for shareholders. The big payments make it more valuable for the executive individually to make a deal and profit all at once, rather than avoid a sale and keep receiving high annual compensation.